Molecules Over MOUs: Japan’s Approaching Supply Stress

How a chokepoint disruption sets the table for visible minimums, yen pressure, and global economic spillovers.

As the conflict in Iran grinds on, the market is moving from headlines about strikes and diplomacy to the harder question that matters for investors: what happens when sustained crude-flow disruption starts to show up in inventories, prices, currencies, and growth?

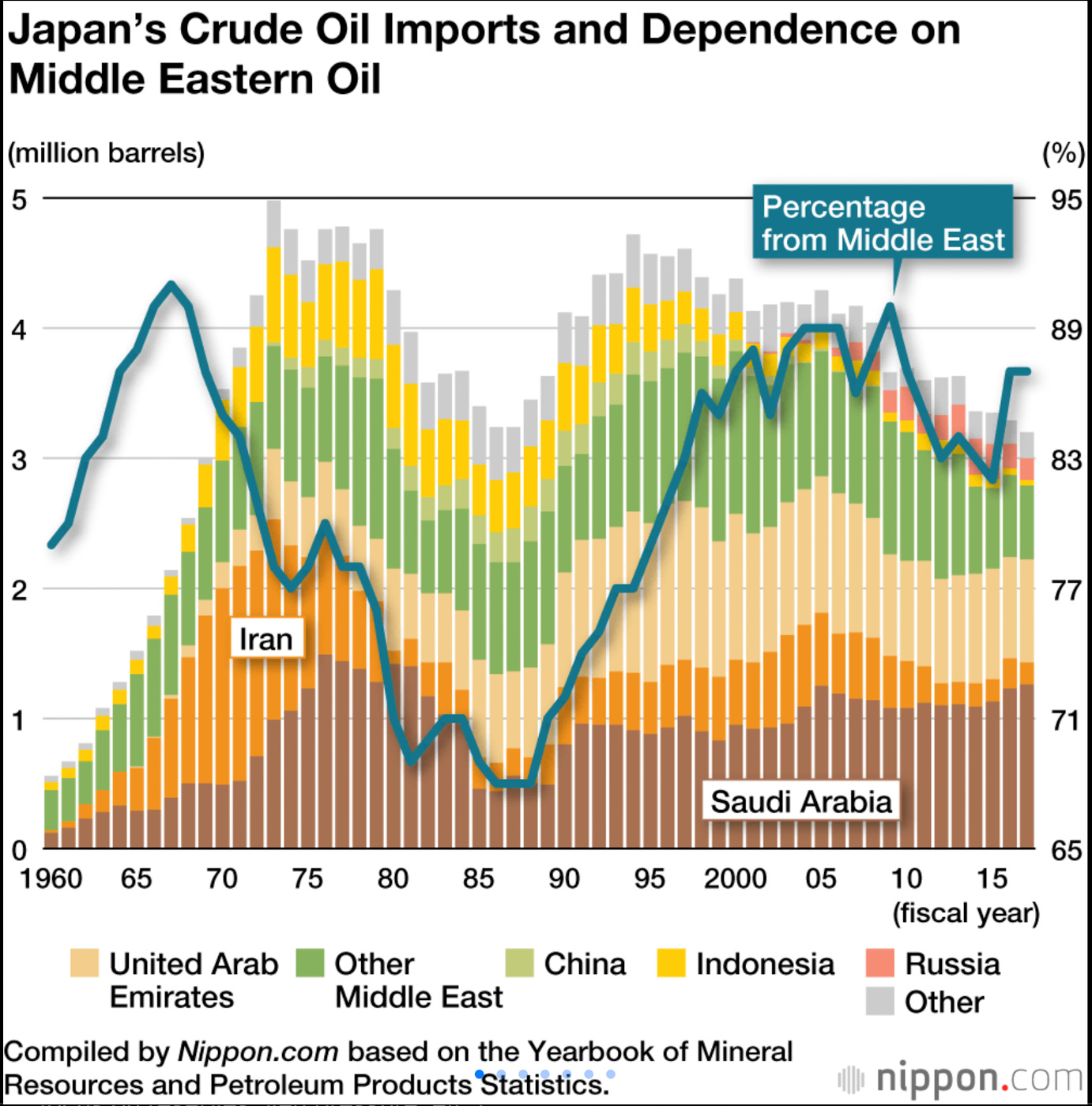

Japan is one of the clearest early casualties. It is the world’s third-largest economy, it relies on imported energy, and roughly 95% of its oil imports come from the Middle East, with a large share of those barrels exposed to the Strait of Hormuz chokepoint. Japan does not need to hit zero imports to become a problem. It only needs the market to realize that physical replacement barrels are slow, expensive, and uncertain, while reserve drawdowns are steadily shortening the bridge to normal supply.

The market sequence

The sequence is straightforward: conflict leads to crude-flow disruption, crude-flow disruption leads to further disruption and reserve drawdowns, reserve drawdowns lead to visible minimums and stress, and visible stress leads to knock-on effects across FX, rates, inflation, and growth.

That is the tradeable setup. Markets are not waiting for literal shortages. They reprice when the probability of shortages becomes visible enough to matter, and Japan is moving into that zone now.

Why Japan matters

Japan is especially vulnerable because it is not just an importer, it is an importer with limited domestic energy production and a large industrial base that is highly sensitive to input costs. The country has already been forced to release oil from reserves, with roughly 80 million barrels tied to emergency measures, and officials have also signaled additional reserve use as the disruption persists. That is important because reserves are intended to be a buffer, not a solution; the longer they are used to plug the gap, the more the market focuses on depletion, replenishment risk, and the possibility of rationing or curtailment later on.

The key point is not whether Japan gets one tanker today or next week. The key point is whether the market believes the supply bridge is getting shorter while replacement flows remain unstable. If the answer is yes, the repricing starts before the shortage becomes visible in physical end-user data.

Macro transmission

That repricing is already visible in the inflation data. Japan’s wholesale inflation accelerated to a three-year high, while the yen-based import price index jumped sharply, with petroleum and related sectors a major driver. At the same time, the Bank of Japan is facing pressure to tighten policy even as energy costs threaten to slow growth, which is a bad mix for an economy already sensitive to imported inflation.

From there, the transmission is classic:

Higher crude prices raise Japan’s import bill.

A larger import bill weakens the yen.

A weaker yen feeds more imported inflation.

More inflation complicates BOJ policy.

Tighter policy into weaker growth raises recession risk.

Higher funding stress and weaker risk sentiment can spill into equities, credit, and the carry trade.

That is why this stops being just an energy story. It becomes a currency story, a rates story, a growth story, and eventually a global risk story.

Tradeable implications

The market implications are likely to show up first in the assets most exposed to imported energy and Japan’s macro balance:

JPY downside risk increases if the market concludes that reserve releases are only delaying a larger import shock.

Japanese government bond yields can face conflicting pressures from higher inflation and weaker growth, especially if the BOJ keeps signaling tightening.

Japanese equities in autos, chemicals, steel, semis, and transport remain vulnerable to higher energy input costs and margin compression.

Global crude remains supported because Japan is not the only import-dependent economy under strain, and any return of Asian spot demand competes for the same constrained barrels.

Broader capital flows can shift if Japanese institutions need to hedge currency exposure or fund higher import costs, adding pressure to global rates and reserve assets.

The endurance trap

This is the endurance trap in action. Iran does not need to keep the Strait closed forever to force a market reaction; it only needs to create enough disruption that insurers, shipping operators, refiners, and investors start to believe the normal flow regime is no longer dependable, or in the case of Japan, will not be restored quickly enough to avert functional disruption.

Even if diplomacy eventually improves the situation, the adjustment is slow. Mine clearance, insurance repricing, tanker repositioning, and new cargo arrivals all take time, and time is the commodity that Japan has even less of as the reserve bridge is being used. Markets, however, do not wait for the physical shortage to become obvious in daily life. They reprice once the probability of stress becomes credible and the knock-on impacts of that stress are identified with conviction.

Japan’s vulnerability is therefore not just about barrels. The conversation has shifted from diplomatic narratives and MOUs to the hard reality of physical supply. What began as an Iran story is now pivoting towards a broader macro event driven by actual barrel shortages. If that shift takes hold, the focus moves beyond crude prices to yen weakness, policy pressure, inflation risks, capital flight, and wider global spillovers.

Because at this stage, supply is not a narrative variable.

It is the constraint.

Disclaimer: This note is provided for informational purposes only and does not constitute investment, financial, or legal advice. The information contained herein is based on current market observations and analysis, which are subject to change without notice. All investments involve risk, including the loss of principal. We do not provide personalized recommendations, and readers should conduct their own due diligence or consult with a qualified professional before making any investment decisions.